Have you ever looked at markets and felt everything seemed calm, while something bigger was actually moving underneath? That is one of the clearest lessons from the IMF’s latest global outlook.

Wars are not only human tragedies. They are also economic shocks. And their effects can spread far beyond the battlefield.

They can hit output, inflation, public debt, trade, exchange rates, capital flows, and even the long-term health of workers and households.

For investors, this matters a lot. Conflict is not just a geopolitical event. It is a macroeconomic force that can change the way entire markets behave.

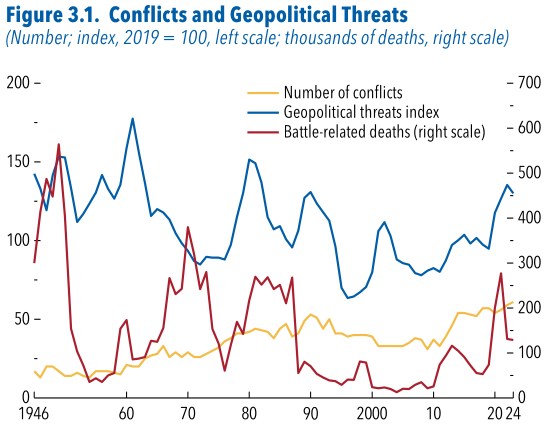

Since the end of the Cold War, the number of active wars has risen again toward levels not seen since World War II. In 2024, more than 35 countries experienced conflict on their own territory. Around 45 percent of the world’s population lived in conflict-affected countries. And since 2010, conflicts have caused more than 1.9 million deaths.

Source: International Monetary Fund, World Economic Outlook (April 2026)

Georeferenced Event Dataset (GED) version 25.1; UCDP/PRIO Armed Conflict Dataset

version 25.1; and IMF staff calculations.

Note: The figure shows the number of conflicts involving the government of at least

one state, based on the UCDP/PRIO dataset. The geopolitical threats index captures

threats related to war, peace, military buildups, nuclear risks, and terror, and is shown

as a three-year moving average. Battle-related deaths are drawn from the PRIO dataset

for 1946–88 and from the GED for 1989–2024. PRIO = Peace Research Institute Oslo;

UCDP = Uppsala Conflict Data Program.

The problem is not only the fighting itself. The bigger problem is what war does to the economy.

Production slows. Trade gets blocked. People move. Investors wait. Governments spend differently. Revenues weaken. Currencies come under pressure. Confidence disappears.

And once confidence disappears, capital often follows it out the door.

That is why the IMF treats conflict as a macroeconomic event, not merely a political one.

For retail investors, this distinction is important. It helps explain why sectors, currencies, sovereign bonds, and frontier-market equities can move so sharply when conflict risk rises.

It also explains why recovery after conflict is rarely smooth.

Think of an economy like a house with many connected rooms. War does not just break one window. It damages the roof, the wiring, the water system, and the foundation at the same time.

That is why the IMF highlights the interaction between supply shocks, demand disruptions, fiscal stress, external imbalances, and long-term scarring.

Once these forces start to interact, the damage can reinforce itself. And because of that, the road back to normal growth is usually slower than people expect.

Why conflict shocks are so powerful

Wars destroy productive capacity in a very direct way.

Physical capital gets damaged. Workers are killed, displaced, or pulled away from civilian activity. Infrastructure breaks down. Transport, energy, communications, and logistics become unreliable. Schools are disrupted. Health outcomes worsen.

The human cost is obvious. But the economic cost is just as large.

On the demand side, households cut spending because incomes fall and uncertainty rises. Firms delay or cancel investment because future returns become harder to predict. Governments often shift spending toward military use.

So the same shock hits both supply and demand at once. That is why wartime recessions are often deeper than ordinary downturns.

The fiscal channel matters too.

When an economy contracts, tax collection weakens. At the same time, spending pressures rise because governments must fund defense, humanitarian relief, and emergency repairs.

The result is a squeeze on public finances. In some cases, governments turn to monetary financing, arrears, capital controls, or debt distress.

The external sector also becomes fragile. Exports fall, imports are compressed, foreign exchange becomes scarce, and capital outflows intensify.

Conflict rarely stays contained in one corner of the economy. It spreads into fiscal balances, currencies, inflation, and reserves.

| Channel | What changes during conflict | Why it matters for you |

|---|---|---|

| Production | Factories, farms, transport, and services are disrupted | Earnings fall and recovery becomes uneven |

| Households | Income, employment, and mobility decline | Consumption weakens and labor markets distort |

| Government | Defense spending rises while tax capacity weakens | Debt and fiscal risk increase |

| External sector | Exports fall, capital exits, FX reserves shrink | Currency risk and inflation pressures rise |

| Human capital | Health, education, and skills suffer | Long-run growth potential gets scarred |

Data based on IMF World Economic Outlook, April 2026.

How big are the losses?

This is where the findings become especially sobering.

On average, conflict-affected economies experience an immediate contraction in output. After that, the losses keep building. Within five years, cumulative output losses are around 7 percent.

And the damage does not stop there. The effects often continue well beyond a decade.

In other words, conflict is not a temporary disturbance. It leaves a long economic shadow.

In many cases, these losses are even larger than those caused by financial crises or severe natural disasters.

For retail investors, this is an important reminder. Geopolitical instability can erase economic value faster, and for longer, than many other major risk events.

The impact also reaches beyond the country at war.

Neighboring countries and key trading partners often slow down too, typically by around 1 percent in the early years.

That may sound small. But in macro terms, it is meaningful.

Supply chains shift. Trade routes adjust. Capital reallocates. Sentiment weakens.

Conflict rarely stays local. It tends to create a ripple effect across entire regions.

Not all conflicts are equal. Larger-scale conflicts, shorter but more intense episodes, and internal conflicts often create deeper losses.

But the real takeaway is simpler than that. Any serious conflict brings economic consequences. And the bigger the disruption, the slower the recovery.

Analysis adapted from IMF World Economic Outlook (April 2026).

What actually happens inside the economy during war?

Investment falls. Private consumption weakens. Exports decline more sharply than imports. Public spending may look stable, but it often shifts toward defense priorities.

Debt rises. Capital controls become more common. Foreign investment declines. Exchange rates weaken. Reserves fall.

Inflation accelerates, sometimes sharply. Within five years, cumulative price increases can become large enough to seriously erode purchasing power.

Why does inflation rise so much?

Because conflict disrupts both supply and demand. Goods become harder to produce and transport. Imports become more expensive. Currency depreciation pushes prices even higher.

And if governments rely on monetary financing, inflation risks become even stronger.

The result can be a feedback loop: weaker output, higher inflation, and falling confidence.

Recent events, such as the economic disruptions after the 2022 war in Ukraine, show how fast output can collapse and how difficult stabilization can be.

Even economies that appear resilient at first can face mounting pressure over time, especially through inflation and labor shortages.

The scars are not only macroeconomic

One of the most important insights is that conflict leaves lasting scars.

Capital stock declines. Employment weakens. Productivity falls.

And the damage is not only economic. Health, education, and human development are also affected.

That means an economy’s long-term growth potential can be permanently reduced.

So investors should be careful about assuming a quick rebound.

Yes, output may recover. But the underlying capacity of the economy may still be damaged.

It is a bit like restarting a damaged engine. It may run again, but not at full strength.

Why peace matters more than optimism

Recovery depends on one critical factor: durable peace.

Without it, economic recovery stays fragile.

History also shows that conflict can return within a few years in a meaningful number of cases.

When peace holds, recovery does happen. But it usually comes slowly, and often unevenly.

Source: IMF World Economic Outlook (2026), post-conflict recovery analysis.

Labor markets tend to recover first. People return to work. Displaced populations begin to come back.

But capital investment and productivity take much longer.

That is because investors need confidence. And confidence needs stability.

That is really the question investors should ask: not whether conflict has ended, but whether stability is credible and sustainable.

What should you, as a retail investor, take away?

Do not underestimate conflict risk.

It can affect valuations, currencies, inflation, and growth.

Do not assume quick recoveries.

Watch policy credibility, institutional strength, and stability.

And look beyond headlines. Follow where capital actually flows.

Because in the end, recovery is not only about rebuilding roads, buildings, and factories.

It is about rebuilding trust.

And trust, once broken, takes time to return.

Source: International Monetary Fund. 2026. World Economic Outlook: Global Economy in the Shadow of War. Washington, DC. April.