Have you ever noticed how the global economy can start to look more stable … and then suddenly, something happens that changes the mood?

That is exactly where we are now.

The OECD’s March 2026 interim report uses a title that says a lot about the moment we are living through: Testing Resilience.

And honestly, that is not just a fancy title.

The world really is being tested.

The conflict in the Middle East has escalated further, and the effects are not only humanitarian. They are economic too. They affect energy, trade, inflation, and ultimately the way families and businesses feel the pressure in daily life.

What makes this even more serious is that the global economy was not weak before the conflict intensified. In fact, it was showing a fairly solid recovery trend.

So the real question is this: what changed, why does it matter, and what does it mean for investors and households?

Before the Shock, the Global Economy Was Holding Up

Before we talk about the conflict, it helps to understand what the global economy looked like just before the storm hit.

Late 2025 and early 2026 were actually not as fragile as many people feared.

Global growth was still running at around 3.25 percent in the second half of 2025. That was stronger than the OECD had expected in its previous outlook.

What supported that strength?

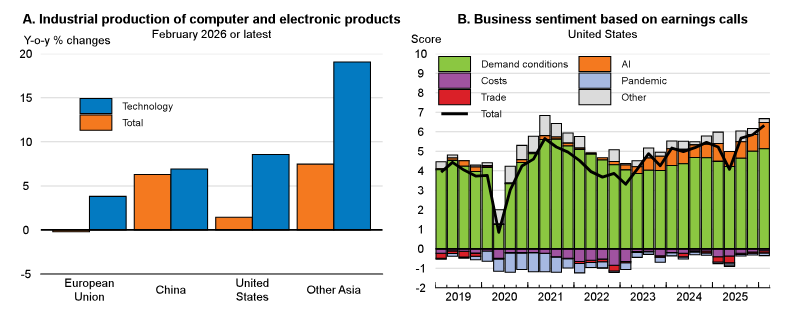

One major answer was AI investment.

Large technology companies in the United States and China kept spending aggressively on artificial intelligence. That spending helped support industrial activity, business optimism, and overall demand.

In other words, the global economy was not just surviving. It was adapting.

Global trade was also improving.

Technology production rose quickly, especially in Asia and the United States. Export activity strengthened. In February 2026, the global manufacturing export orders PMI reached its highest level since November 2021.

That is not a weak backdrop.

It means the world had some momentum before the geopolitical shock arrived.

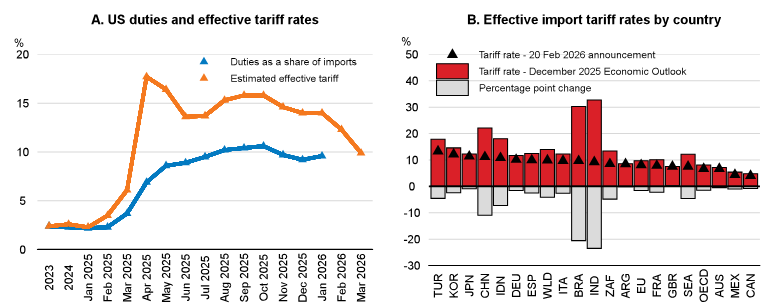

There was also some relief on the trade policy side.

After the US Supreme Court ruled that the International Emergency Economic Powers Act did not authorize tariffs in that way, the expected effective US tariff rate on imports fell from around 14 percent to about 9.9 percent.

That is a meaningful shift, especially for emerging markets like Brazil, China, India, and Indonesia.

But even after the decline, tariffs were still well above pre-2025 levels. So the trade environment was still far from normal.

Then the Middle East Conflict Intensified

Now comes the turning point.

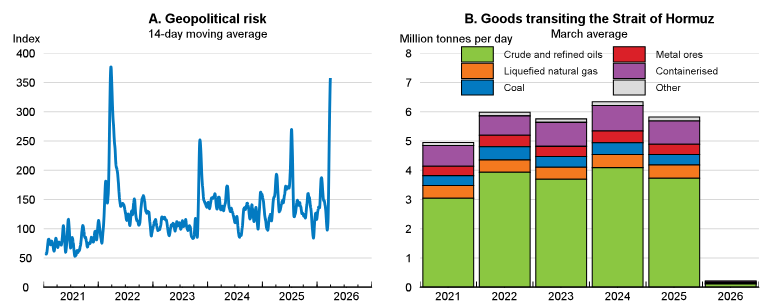

In late February 2026, the conflict in the Middle East intensified sharply.

And the shock was immediate.

The first and most visible impact was energy.

Why energy?

Because the conflict caused serious disruptions to energy infrastructure and shipping routes, especially through the Strait of Hormuz.

And this is important. The Strait of Hormuz is not just any shipping lane.

According to the International Energy Agency, around 20 percent of global oil and petroleum product production passed through the strait in 2025, along with roughly 25 percent of global seaborne oil trade.

For LNG, the dependence is also huge. Around 93 percent of Qatar’s exports and 96 percent of the UAE’s exports move through this route.

That is massive.

And there is no easy alternative route that can handle that volume.

As a result, energy prices jumped fast.

Crude oil rose by more than 50 percent.

Gas prices surged in both Europe and Asia.

Jet fuel and diesel also moved higher.

This happened at a bad time.

Inflation was still above target in several major economies, including Brazil, Mexico, Turkey, the UK, and the US.

So the shock was not arriving in a calm environment. It was landing on top of an already sensitive one.

And that is usually when trouble gets bigger.

Medium-term inflation expectations also started to rise, especially in the euro area and the UK.

That matters because expectations can become self-fulfilling.

If households and businesses believe prices will keep rising, they may act in ways that push prices even higher.

That is how an energy shock can become a broader inflation problem.

Who Gets Hit the Hardest?

Not every country feels this shock in the same way.

Some are far more exposed than others.

Countries that depend heavily on energy imports from the Middle East are the most vulnerable.

Many Asian economies fall into that group.

Japan and Korea, for example, depend on net energy imports for more than 80 percent of total domestic energy use. Much of that supply comes from the Middle East.

So if the supply chain is disrupted, they feel it directly.

Households are also affected differently depending on income.

Energy spending takes a larger share of the budget for lower-income households than for richer ones.

That is why energy shocks are not just macroeconomic events. They are also social events.

When prices rise, poorer families are hit harder.

Businesses feel it too.

Transport, petrochemicals, and metal manufacturing are among the most exposed sectors because they use a lot of energy.

Therefore, the impact spreads beyond oil and gas companies. It reaches the real economy.

The Shock Does Not Stop at Energy

Here is where things become even more interesting.

The conflict does not only affect energy.

It also affects other commodities and supply chains.

Take fertilizers, for example.

Persian Gulf countries accounted for a large share of global fertilizer exports in 2024, including urea, diammonium phosphate, and anhydrous ammonia.

And LNG is also a key input for nitrogen-based fertilizers.

That means the energy shock can quickly become a food shock later on.

Fertilizer prices had already risen by more than 40 percent since mid-February.

If the disruption continues, global food prices could rise in 2027.

That would matter for countries like Brazil, India, Australia, and South Africa, which rely heavily on fertilizer imports from the Middle East.

Now look at aluminium, helium, and bromine.

Gulf countries account for a meaningful share of global primary aluminium supply. They also produce a very large share of helium and bromine.

Why should you care?

Because helium and bromine are important in semiconductor and memory-chip supply chains.

So yes, even the technology industry can feel the pressure.

Logistics and air travel also face disruption.

Airlines based in the Persian Gulf account for a meaningful share of global cargo and passenger traffic.

If air routes are restricted, trade costs rise and shipping patterns become less efficient.

In short, the shock spreads.

Not just through energy. Through the entire supply chain.

What the OECD Projects Now

So what do the numbers say now?

The OECD projects global GDP growth at 2.9 percent in 2026 and 3.0 percent in 2027.

That sounds okay at first glance.

But the context matters.

Before the conflict intensified, 2026 growth had been expected to be about 0.3 percentage points higher.

That gain has now been wiped out.

So the world has not only lost momentum. It has also lost some of the optimism that was building before the shock.

Country projections show the same pattern.

| Country / Region | 2026 Outlook | Main Pressure | What It Means |

|---|---|---|---|

| United States | Growth slows to 2.0% | Weaker real income and spending | AI still supports growth, but consumers are less strong |

| Euro Area | Growth slows to 0.8% | Energy and inflation pressure | Defense spending may help later |

| China | Growth slows to 4.4% | Higher energy costs and property adjustment | Still growing, but under pressure |

| India | Growth slows to 6.1% | Gas supply restrictions | Production activity may be disrupted |

Inflation is also moving higher.

G20 inflation is projected to rise from 3.4 percent in 2025 to 4.0 percent in 2026.

That is a big upward revision.

For the US, inflation is expected to rise from 2.6 percent in 2025 to 4.2 percent in 2026.

Then, if energy pressures ease, inflation may fall again in 2027.

But that depends on what happens next.

What If Things Get Worse?

OECD also gives scenario analysis. And this is where the picture becomes even clearer.

In the downside scenario, energy prices rise even further.

Oil could average USD 135 per barrel in the second quarter of 2026. European gas prices could also stay elevated.

If that happens, global output could fall by around 0.5 percent in the second year, while consumer prices rise by around 0.9 percent.

Asia-Pacific economies would be hit hardest because of their import dependence.

Policy rates could also rise by 25 to 50 basis points in many countries.

And that is before even considering the possibility of energy rationing.

On the other hand, the upside scenario is much better.

If the conflict ends sooner and energy prices return to pre-conflict levels, global output could rise by about 0.3 percent in the second year, while consumer prices could fall by around 0.7 percent.

So the direction of the world economy still depends heavily on geopolitics.

What Policymakers Should Do

Now the policy part.

Central banks need to stay alert.

They need to watch inflation expectations carefully and avoid overreacting to supply shocks unless the shock starts spreading more broadly into wages and domestic inflation.

That balance is not easy.

Some countries may keep rates unchanged. Others may need small increases or later cuts, depending on how inflation develops.

Fiscal policy should also be targeted.

Governments may need to support vulnerable households and viable businesses. But support should not be too broad, too expensive, or too permanent.

Why?

Because broad subsidies can become expensive very quickly and may reduce the incentive to save energy.

Trade policy should also avoid making the problem worse.

Export restrictions usually increase scarcity and push prices even higher.

That helps no one in the long run.

Medium-term energy efficiency is also essential.

Countries need to reduce dependence on imported fossil fuels and invest more in energy-efficient systems, buildings, transport, and industrial equipment.

That is the real structural answer.

Not just short-term relief. Long-term resilience.

Lessons From 2022–2023 Still Matter

The recent past already taught us something important.

After the energy shock following Russia’s invasion of Ukraine, governments learned how hard it is to design support that is both targeted and efficient.

There were two big lessons.

First, it is difficult to identify exactly which households and businesses need help the most in real time.

Second, it is difficult to support people without weakening incentives to save energy.

That is why policy design matters so much.

You do not just want aid. You want smart aid.

That means targeted support, clear expiration dates, and better energy-saving incentives.

A Bit of Hope Still Remains

Even with all these risks, there is still a reason not to be completely pessimistic.

Businesses have shown strong adaptation in recent years. They have already dealt with higher trade barriers, inflation spikes, and labor shortages.

So it is possible they will adapt again.

AI investment is another positive force.

In the US, productivity gains appear stronger in sectors that have adopted AI more aggressively, such as finance and professional services.

If those gains become broad and durable, they could support future growth.

That is not a guarantee.

But it is a meaningful offset.

And other countries may eventually increase their own AI-related investment too.

So the story is not only about shocks. It is also about adaptation.

What This Means for Retail Investors

If you are a retail investor, this is not the kind of story you should ignore.

Why?

Because macro shocks can change sector performance very quickly.

Energy producers may benefit.

Transportation, manufacturing, and chemicals may face margin pressure.

Consumer sectors may weaken if household purchasing power is squeezed.

Inflation-sensitive assets may react differently depending on central bank policy.

So the question is not just, “What happened?”

The better question is: “Which companies and sectors can survive this environment?”

Can they pass on costs? Can they absorb higher fuel prices? Can they keep margins intact?

That is where investor thinking becomes practical.

In times like this, prediction is useful. But preparation is better.

A Simple Way to Read the Situation

To make it clearer, here is a simple framework.

Higher energy prices can help energy producers, but hurt energy users.

Inflation pressure can weaken consumer spending and increase policy uncertainty.

Supply chain stress can create winners and losers across industries.

Government and central bank responses can either soften the shock or make it worse.

So this is not just an economic story.

It is also a portfolio story.

Closing Thoughts

The world is not collapsing. But it is under pressure.

That difference matters.

A resilient economy can still slow down. A strong market can still become volatile. A good company can still suffer when the macro environment turns unfriendly.

That is why the most useful response is to stay informed, stay selective, and stay disciplined.

Because in periods like this, resilience is not just a macroeconomic word.

It is an investment strategy.

So if you are managing a portfolio, keep asking the right questions. Which sectors benefit from the shock? Which sectors are exposed? Which companies can absorb higher costs? Which ones cannot?

Those questions may not give you an instant answer. But they will help you think more clearly.

And in uncertain markets, clarity is often more valuable than excitement.