For decades, the big story in commodities was simple. Who controls oil, gas, and coal? That question shaped geopolitics, national power, and investment returns for an entire generation.

Now the story is changing. Fast.

Today, the market is paying more attention to minerals like lithium, nickel, cobalt, graphite, and rare earths. Why? Because these materials sit at the center of electric vehicles, batteries, grid storage, semiconductors, renewable systems, and defense technology. The International Energy Agency reported that lithium demand rose by nearly 30% in 2024, while nickel, cobalt, graphite, and rare earths each grew by 6–8%. That is not a minor shift. That is the beginning of a new commodity cycle.

So, is fossil fuel really disappearing? Not necessarily. Oil and gas still matter. But the investment excitement is moving somewhere else. And for retail investors, that matters a lot. Because of that, the opportunity set is no longer limited to barrels and pipelines. It now includes mine operators, refiners, processors, battery-material suppliers, and recycling businesses. Therefore, the real question becomes: where does the value accumulate in the new commodity economy?

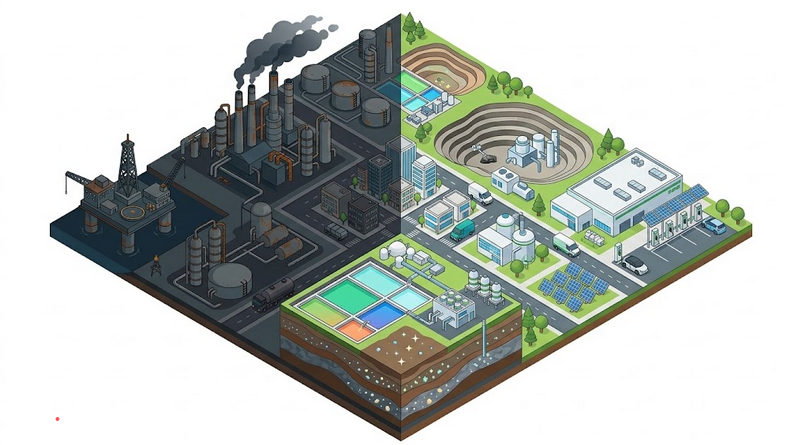

To make it clearer, think of the old economy like a kitchen powered by gas. The new economy is more like a house wired with electricity, packed with devices, sensors, batteries, and chargers. Different system. Different bottlenecks. Different winners.

Why the market is shifting away from fossil fuels

The shift is happening because the global economy is changing its energy plumbing. Electric vehicles need batteries. Batteries need minerals. Grid expansion needs copper. Wind and advanced electronics need rare earths and specialty metals. In other words, the energy transition does not remove commodity demand. It redistributes it.

The IEA’s 2025 Global Critical Minerals Outlook also showed something important: despite strong demand growth, investment momentum weakened in 2024. Spending rose only 5%, down from 14% in 2023, and real investment growth was just 2% after inflation. Exploration also plateaued. Why does that matter? Because it suggests the market may still be underinvesting in the supply chain that the future depends on.

This is important for you as an investor. When demand rises faster than supply investment, scarcity tends to appear later. And scarcity is where pricing power often shows up. Not immediately. Not in a straight line. But eventually.

On the contrary, when everyone assumes supply will arrive smoothly, capital often chases the wrong thing at the wrong time. That is why commodity cycles are so difficult. The best returns usually appear when the story is still being dismissed.

The main forces behind the critical mineral boom

1. Electrification is multiplying mineral demand

EVs are the clearest example. A battery-powered car is not just a car with a new engine. It is a different industrial machine. It requires lithium, nickel, cobalt, graphite, manganese, copper, and often rare-earth-based components in the supply chain.

The IEA says clean energy technologies could more than double total mineral demand by 2040 in its stated policies scenario, and quadruple it in a more ambitious scenario. It also says EVs and battery storage are responsible for roughly half of the growth in mineral demand from clean energy technologies.

That is a huge deal. Because of that, minerals that once looked ordinary are now strategic. Lithium is no longer just a niche industrial input. Nickel is no longer just a metal for stainless steel. Cobalt is no longer just a byproduct. These materials are now part of the infrastructure of electrification.

2. Supply is concentrated in a few countries

This is where the story becomes more interesting. Demand is spreading globally, but supply is not.

The IEA reported that the average market share of the top three refining nations for key energy minerals rose from about 82% in 2020 to 86% in 2024. It also said that around 90% of supply growth came from a single leading supplier in each of several markets: Indonesia for nickel, and China for cobalt, graphite, and rare earths.

That level of concentration is not just a market statistic. It is a geopolitical warning light. If one country dominates refining, processing, or exports, then everyone else becomes exposed to price swings, policy shifts, logistics disruptions, and trade restrictions.

Think of it like one bakery supplying bread to an entire city. If that bakery slows down, raises prices, or shuts its doors for a week, everyone feels it. The same logic applies to mineral supply chains—only the scale is much bigger.

3. Governments now treat minerals as strategic assets

Minerals are no longer being viewed as simple industrial goods. They are now treated as national security assets.

The USGS 2025 Mineral Commodity Summaries shows that the United States was 100% net import reliant for 12 of the 50 individually listed critical minerals, and more than 50% reliant for 28 more. The same report notes that China was the leading producing country for 30 of 44 critical minerals for which reliable estimates were available.

What does that tell you? The world is not just trying to build more mines. It is trying to build resilience. Because once a supply chain becomes strategic, the policy response changes. Subsidies appear. Export controls appear. Permitting gets faster in some places and slower in others. The market becomes more political.

As a result, investing in commodities is no longer just about extracting rocks from the ground. It is about understanding policy, processing capacity, logistics, and geopolitical leverage.

4. Fossil fuels are still important, but the growth narrative is moving

This does not mean oil and gas have no future. They still power transport, industry, petrochemicals, and large parts of the global economy. But the growth narrative is increasingly different.

In many markets, the big long-term excitement is shifting toward electrification, storage, advanced manufacturing, and energy security. That means the commodity conversation is moving from “How much energy do we burn?” to “What materials do we need to build and store energy?” That is a profound change.

Why retail investors should pay attention now

Here is the opportunity. The market often focuses on the end product—an EV, a battery, a wind farm, a smartphone. But the durable value can sit upstream, in the bottlenecks.

That is why mineral investors do not need to think only about “buying a mineral.” They can also look at the companies that mine it, refine it, transport it, recycle it, or provide the technology that makes the supply chain work. In many cycles, the best risk-adjusted returns come from the bottleneck, not the headline.

But there is a catch. Commodity investing is never a straight line. Prices can rise sharply and then fall hard. In fact, the IEA reported that lithium prices fell by more than 80% from 2023 levels after surging eightfold in 2021–2022, while graphite, cobalt, and nickel prices also declined in 2024.

So the lesson is not “buy anything linked to critical minerals.” The lesson is to understand the cycle. Because of that, timing, quality, and discipline matter more than excitement.

Imagine buying a shovel store during a gold rush. That sounds great. But not every shovel store is in the right location, not every supplier has margins, and not every rush lasts as long as people think. The same is true here.

The key mineral themes investors are watching

1. Nickel: the battery metal with industrial depth

Nickel matters for two reasons. First, it is used in stainless steel and many industrial applications. Second, it is a key battery metal in some chemistries, especially those that need higher energy density.

Indonesia is central here. USGS data show Indonesia produced about 2.2 million metric tons of nickel in 2024 and had estimated nickel reserves of 55 million metric tons. The IEA also says Indonesia was the dominant source of growth in refined nickel supply from 2020 to 2024.

What does this mean for investors? It means nickel is not just a price chart. It is a policy story, an industrial story, and a country-level strategy story. That is why Indonesia has become one of the most important names in the new commodity map.

2. Cobalt: essential, but tightly linked to supply concentration

Cobalt remains a highly strategic mineral, even as battery chemistry evolves. Why? Because it still matters in metallurgy and certain battery formulations, and because its supply chain is extremely concentrated.

The USGS reported that Congo (Kinshasa) accounted for about 76% of world cobalt mine production in 2024, while Indonesia increased cobalt mine production by 47% that year. It also noted that much of the output was shipped to China for processing, and China increased cobalt refinery capacity in 2024.

That combination—high concentration plus processing dependence—is exactly what investors should pay attention to. Not necessarily because cobalt is guaranteed to soar, but because supply chain fragility can create both opportunity and volatility.

3. Rare earths: small volumes, huge strategic importance

Rare earths are a perfect example of why “small” does not mean “unimportant.” The USGS lists rare earths as critical to permanent magnets, and it notes that materials such as neodymium, praseodymium, dysprosium, terbium, and others are tied to magnets and other high-value applications.

Why should that matter to you? Because permanent magnets are not optional in many advanced technologies. They are one of the hidden inputs that make modern electrification and advanced electronics work.

And again, the supply chain is concentrated. The USGS says China was the leading producing country for many critical minerals, including rare earths, and the IEA says China remains dominant in refining and processing for several key mineral categories.

4. Copper: the quiet giant

Copper does not always get the same attention as lithium or rare earths. But it should.

The IEA says copper demand is being pushed by grid investment and electrification, and that supply could face a major shortfall by 2035 if the project pipeline does not improve. Copper is everywhere in the new economy: wiring, grids, chargers, motors, and data infrastructure.

In simple terms, copper is like the plumbing of electrification. You may not notice it when it works. But you notice it very quickly when it is missing.

What this means for the investment thesis

Here is the practical takeaway. The best investment idea is not “commodities are going up.” That is too vague. The better idea is: the world is rebuilding energy and industrial systems, and that rebuild needs specific minerals, specific processing capacity, and specific infrastructure.

Therefore, investors should think in layers:

First, the mine. This is the most visible part, but also the most operationally risky. Grade, extraction cost, permitting, politics, and capex all matter.

Second, the processor or refiner. This is often where leverage sits. The IEA’s data on concentration show that refining has become more concentrated, not less.

Third, the recycler. As supply chains mature, recycled material can become a meaningful competitive advantage, especially where policy favors secure and local sourcing.

Fourth, the enabler. Think of equipment, engineering, logistics, testing, and materials technology. These companies may not mine the metal, but they help control cost, recovery, and throughput.

Most importantly, not every “critical mineral” story deserves a premium valuation. A good story is not the same as a good business. That distinction matters.

Indonesia’s rise in the new commodity map

Indonesia is one of the clearest examples of the new mineral era.

For years, the country was seen mainly as a raw-material exporter. But nickel changed the conversation. With large reserves, strong production growth, and expanding downstream processing, Indonesia moved closer to the center of battery supply chains. USGS data show substantial 2024 nickel output and a large reserve base, while the IEA highlights Indonesia as the top single supplier behind much of the recent growth in refined nickel supply.

That is not just an industrial shift. It is an investment lesson. Countries that can move from raw extraction to processing and downstream manufacturing often capture more value. In other words, the money is not only in the hole in the ground. The money is in the next step after the hole.

At the same time, the story also carries a warning. More processing means more capital, more regulation, more environmental scrutiny, and more execution risk. That is why the opportunity is real, but never simple.

The biggest mistakes retail investors make

The first mistake is chasing headlines. A mineral becomes “hot,” and suddenly every related stock looks attractive. That is usually when discipline matters most.

The second mistake is ignoring the cycle. The IEA shows that battery-metal prices already cooled sharply after the 2021–2022 surge. That means buying after a huge story has already been priced in can be dangerous.

The third mistake is treating all minerals the same. They are not the same. Some are more cyclical. Some are more concentrated. Some have easier substitution. Some are byproducts, which means supply can be slow to respond even if prices rise.

The fourth mistake is focusing only on demand and ignoring processing. If the mine is in one place and the refining is controlled somewhere else, the real bottleneck may not be where you think it is.

The fifth mistake is forgetting policy risk. Export restrictions, tariffs, sanctions, local content rules, and environmental permitting can change the economics very quickly.

A smarter way to approach the theme

So what should you do with all this information?

Start with a simple framework. Ask five questions before you invest in any mineral-linked opportunity:

1. Is the mineral truly strategic, or just temporarily popular?

2. Does the company control low-cost supply, processing, or a scarce technology?

3. Is the supply chain concentrated enough to create pricing power, or is it too crowded?

4. Does the investment rely on a single policy trend, or can it survive different scenarios?

5. Is the valuation still reasonable after the market’s enthusiasm?

This is important. A good commodity theme does not mean every asset in that theme is good. In fact, the better the theme, the more important selection becomes.

Another practical approach is to diversify across the value chain. One company may offer exposure to mining. Another may offer exposure to processing. A third may benefit from recycling or equipment demand. That way, you are not dependent on just one operating model.

And most importantly, think in time horizons. The mineral transition is not a one-quarter story. It is a multi-year industrial reconfiguration. Therefore, patience matters almost as much as analysis.

Closing: the next commodity cycle is already forming

The world is not leaving commodities behind. It is entering a different commodity era.

The old era was built on fossil fuels. The new era is being built on critical minerals, processing capacity, and supply chain control. That does not mean the old assets vanish overnight. It means the most interesting growth, the most strategic bottlenecks, and some of the most important policy decisions are shifting elsewhere.

For retail investors, the message is simple. Do not look only at what the world consumes today. Look at what the world must build next. Because of that, the most valuable resources of this decade may not be the ones that powered the last one.

And that is the real story. Not just a new set of metals. A new map of power, profits, and opportunity.

Source: USGS – Mineral Commodity Summaries 2025

Source: IEA – Global Critical Minerals Outlook 2025 Executive Summary