Autonomous vehicles are no longer just about passenger cars.

That is the part many investors still miss. The real opportunity is broader, less flashy, and arguably more important. Think of truck platooning on highways. Think of ships that can navigate with far less human input. Think of heavy equipment that can move mountains of rock in a mine while the operator sits far away—or does not sit there at all. The problem is not whether the technology exists. The problem is whether the economics, regulation, and operating environment are ready. And in several niches, they already are. McKinsey estimates autonomous trucks could support an approximately $600 billion market by 2035, while also cutting total cost of ownership on long-haul routes by 42% per mile in its model. At the same time, Europe’s land-transport labor market is still tight, with 233,000 unfilled truck-driver jobs in 2023 and 62% of trucking companies reporting severe recruiting challenges. Source : McKinsey — Will autonomy usher in the future of truck freight transportation?

So what does that mean for you as a retail investor?

It means this theme is not a single-stock story. It is a chain reaction story. The winners are likely to be the companies that sell AI, sensors, fleet software, control systems, industrial automation, and specialized vehicles for mining, logistics, and maritime use. The pressure, on the contrary, lands on labor-intensive transport models that depend on scarce drivers and thin margins. Therefore, the key question is not “Will autonomy happen?” It is “Where does autonomy become commercially useful first?”

Autonomous Vehicles Beyond Cars: Why This Trend Matters

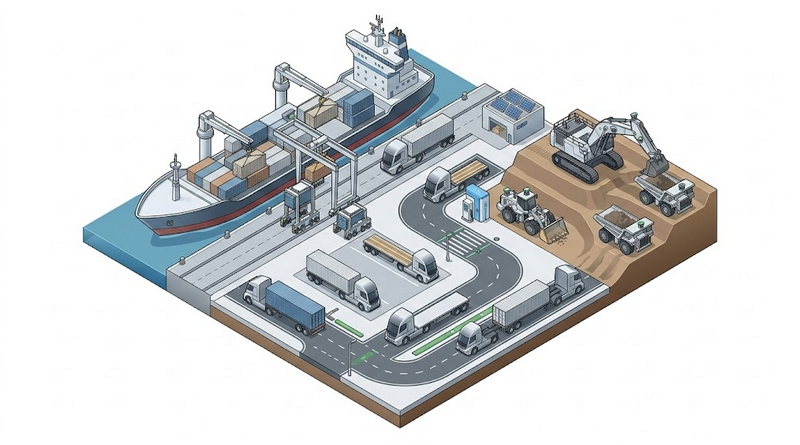

When people hear “autonomous vehicle,” they usually picture a robotaxi in a city. That is only one slice of the picture. In many ways, the easier and more profitable use cases are elsewhere. Closed environments like mines, ports, warehouses, and fixed highway corridors are simpler than urban streets. Fewer edge cases. Clearer routes. More predictable traffic. Better maps. More control. In other words, this is not about teaching a machine to survive chaotic downtown traffic before lunch. It is about teaching it to do the same route again and again, safely, with high utilization. That is a very different game. The World Economic Forum notes that early deployments are already on the road, but large-scale rollout will take longer than many once expected, and it explicitly frames autonomous trucks as one of the main autonomy use cases between 2025 and 2035. Source :

And that is exactly why the “beyond cars” segment matters. A truck that moves freight more hours per day can create real savings. A ship that reduces crew dependence can improve route flexibility. A mine truck that removes people from hazardous zones can improve safety. Not necessarily glamorous. But very investable if the unit economics improve.

Why Autonomous Trucks, Ships, and Heavy Equipment Are Gaining Attention

1. Driver shortages are not a temporary headline

This is important. The labor shortage in transport is not just a short-term wage problem. It is structural. Europe’s road freight sector had 233,000 unfilled truck-driver positions in 2023, and the shortage is expected to worsen if aging workers retire faster than younger workers enter the field. For companies running large fleets, that means capacity constraints, higher wages, more overtime, and more fragile logistics. Because of that, autonomy starts to look less like a science project and more like a supply-chain workaround.

2. The first wins come from predictable routes

Autonomy works best where the environment is bounded. Mines have controlled routes. Warehouses have mapped aisles. Port-to-port shipping has defined corridors. Hub-to-hub trucking can be designed around repeatable lanes. On the contrary, the hardest environments are dense city streets with pedestrians, motorcycles, traffic changes, weather surprises, and construction. Therefore, the first commercial wave is not likely to be “everywhere at once.” It is likely to be “here first, then there.”

3. The economics improve when vehicles run more hours

Think of a truck like a coffee machine in a busy office. The more people use it without wasting time, the more value it creates. Autonomous fleets can, in theory, spend less time idle and more time moving. McKinsey’s 2024 analysis suggests long-haul autonomous trucking can deliver substantial total-cost-of-ownership savings on routes above 1,500 miles, because driver costs, fuel use, and accident-related costs can be reduced. That is why investors should pay attention to utilization rates, not just flashy demo videos.

4. Sensors, AI, and control software are finally mature enough

Autonomy is not one invention. It is a stack. Sensors. Radar. Cameras. Mapping. Decision software. Redundant braking and steering. Remote monitoring. Fleet orchestration. A single weak link can slow everything down. But the stack is becoming stronger, cheaper, and more specialized. That is why industrial autonomy is now moving from “possible” to “piloted,” and in a few cases, to “commercial.”

5. Regulation is opening the door in specific corridors

The most practical autonomy projects are often built around regulations that allow defined routes, safety supervision, or controlled trials. Germany already allows driverless driving on defined routes with technical supervision, and MAN says further customer transport projects from 2025 will drive development toward series application. That matters because the technology roadmap and the legal roadmap are now beginning to meet each other. source : World Economic Forum — Autonomous Vehicles: Timeline and Roadmap Ahead

Who Is Already Exploring This in Europe and Asia?

Let’s make it clearer with real companies. These are not fantasies. These are publicly traded or major listed groups already testing autonomy in transport and industrial use cases. Some are still in pilot mode. Some are already commercial in narrow environments. That distinction matters. A lot.

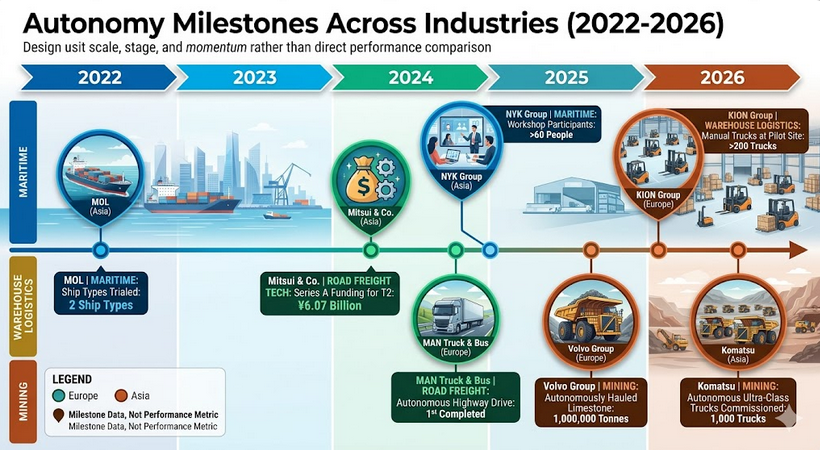

Europe: Volvo Group has reached a major milestone at Brønnøy Kalk in Norway, hauling over one million tonnes of limestone autonomously with seven Volvo FH trucks over a five-kilometre route. KION Group has deployed its first AI-supported autonomous industrial truck at a GXO warehouse in Épinoy, France, where the site still operates more than 200 manual trucks. MAN Truck & Bus reports that it has successfully completed the first highway drive of an autonomous truck in Germany, with hub-to-hub customer tests planned from 2025. Scania says autonomous vehicles are already being tested on public roads in Europe, with hub-to-hub logistics as a key near-term use case. Source : Volvo Group — Volvo achieves milestone with over 1 million tonnes hauled autonomously at Brønnøy Kalk

Asia: Komatsu has crossed a major threshold by commissioning its 1,000th autonomous ultra-class haul truck, and it has been commercially operating autonomous haulage since 2008. NYK Group is advancing maritime autonomous surface ship trials with the Maritime and Port Authority of Singapore, with a joint workshop attended by more than 60 participants and a clear focus on interoperability with port systems. MOL says it completed the world’s first successful sea trial of unmanned ship operation from port to port, and it used two ship types in the project, including automated mooring tests. Mitsui & Co. is also active: its DX materials say it is aiming to develop Level 4 autonomous truck technology and is conducting public-road verification tests through T2. :source : Komatsu — FrontRunner Autonomous Haulage System milestone

A bar chart works well for the “scale” rows like Volvo, Komatsu, and Mitsui. A timeline works better for the “firsts” and “pilot” rows like MAN, NYK, and MOL. If you want a source image graph from another outlet, McKinsey’s TCO chart for autonomous heavy-duty trucks is especially useful because it visually explains the cost logic behind the theme. The World Economic Forum white paper is also a good source for timeline framing.

What This Means for Retail Investors

Here is the practical part. Do not buy the story just because it sounds futuristic. Buy the evidence. That means watching where autonomy is already moving from pilot to paid service, where safety drivers are being removed, and where routes are becoming repeatable enough for scale. Volvo’s Brønnøy Kalk project is a strong example of a commercial environment that has already crossed the “demo” stage. Komatsu’s 1,000-truck milestone is even more important because scale matters in industrial automation. KION’s warehouse deployment matters because warehouses are often the first place where physical AI can become real revenue. Source : KION Group — First AI-supported autonomous industrial truck at GXO warehouse

On the contrary, not every autonomy headline deserves the same valuation premium. A concept truck is not the same as a fleet with paid utilization. A ship trial is not the same as a global autonomous shipping network. A proof-of-concept in a mine is not the same as a city operating system. Therefore, investors should separate “technology validation” from “commercial penetration.” That is the difference between excitement and actual earnings power.

The second thing to watch is geography. McKinsey projects Europe may still lag the U.S. in autonomous heavy-duty truck penetration by 2035, partly because Europe has more complex roads, tunnels, snow, and shorter average routes. Yet Europe could still capture meaningful value because the TCO savings can be large. In other words, slow adoption does not mean no investment case. It just means the winners may be more selective.

The third thing to watch is ecosystem fit. Autonomy beyond cars does not live alone. It needs sensors, controls, mapping, fleet software, maintenance systems, and often port or warehouse integration. That is why this theme often rewards boring-looking companies as much as flashy ones. The machine itself is only part of the story. The software stack around it is where durable value can accumulate.

5. The Bottom Line

Autonomous vehicles beyond cars are not a distant fantasy anymore. They are a stepwise industrial transition. Start in closed spaces. Move into hub-to-hub corridors. Expand into port systems and maritime logistics. Then, gradually, push outward. This is not necessarily a revolution that happens all at once. It is more like a slow leak in the old operating model—until one day, the economics look different.

For you as an investor, that means the smartest move is to track milestones, not slogans. Watch for commercial deployments. Watch for route expansion. Watch for safety-driver removal. Watch for revenue tied to autonomy, not only R&D spend. Most importantly, watch which companies are building the platform layer underneath the future of logistics.

Because of that, autonomous vehicles beyond cars may become one of the most practical AI stories in the market. Not the loudest. Not the most glamorous. But perhaps one of the most economically useful. And in investing, useful often becomes valuable.